In the Long Run, We Are All Dead: The Fate of Passive Retail Liquidity Provision in Uniswap v3

Uniswap’s shift from v2 to v3 was an epochal moment in DeFi, with consequences that the crypto world hasn’t yet fully grasped. That update brought markedly greater capital efficiency for buyers, but the brave new world it ushered in has had negative consequences for many liquidity providers. In particular, the claim that v3 is better for passive liquidity providers, or LPs, will be contested in this article by exploring a series of trends related to v3 liquidity providers (with particular focus on passive and retail LPs). Some initial understanding of AMMs and features of the ETH base layer is assumed, but nothing beyond that is required. What follows is a relatively non-technical exploration of certain externalities of v3: the gold standard of more technical explanations is Guillaume Lambert’s many-part series on Uniswap v3, which is significantly heavier on mathematical derivations but abstains from more empirical analysis of the ramifications of v3. The latter, which is the subject of this article, turns out to be a particularly labyrinthine topic, but some conclusions can be drawn all the same.

Very briefly, our verdict will be as follows: Uni v3 chokes out small, passive providers at the same time as it benefits swappers, and absent the further developments of certain tools that can preserve their profitability, we can expect to see an exodus of passive LPs from v3 in the long term until the impermanent loss-adjusted transaction fees are arbitraged back up to 4-5%. As a rule, while solutions to this problem are theoretically capable of aiding LPs (especially if Uniswap migrates to Optimism) they lack both empirical evidence of efficacy and any kind of clean integration with v3, rendering them uncertain and unwieldy. As the Uniswap team shows no intention of encouraging the development of these tools or integrating them into v3, the medium-term secular decline of decentralized liquidity is rendered a fait accompli.

Analyzing the future of passive retail liquidity provision on v3 is only possible with an adequate understanding of the minimum opportunity cost incurred by LP’ing, which is simply not receiving the risk-free rate in DeFi. By arming ourselves with a rough understanding of what the risk-free rate in crypto is, we will then be in a position to discuss v3 mechanics in the abstract, the empirical reality of providing liquidity on v3, and the game-theoretical state of affairs that we can expect to emerge as time progresses. We’ll take a look at a variety of proposed solutions and their deficiencies, before critiquing Uniswap’s stance towards passive LPs for exacerbating the issue. We conclude by briefly proposing further research, most of it empirical backtesting of specific protocols which claim to protect LPs against the ravages of impermanent loss.

I post long-form weekly content on this Substack. Feel free to subscribe, and/or follow me on Twitter: @semajeth.

—

Determinism and the Risk-Free Rate in Crypto

Assessing risk is only possible in a world whose future at least partially resembles its past: in a world with zero tendencies towards repetition, completely absent of laws of nature, calculating risk would be simply impossible. On the other hand, risk isn’t a meaningful concept in a perfectly deterministic world, since there is no uncertainty that could constitute its possibility. Our world, of course, lies between these two extremes, as do all of its financial markets, but their relative location on the spectrum of determinism can vary dramatically. While crypto has certain demonstrable tendencies, such as the historically cyclical nature of its market cycles, it remains more distant from a deterministic world than virtually every other traditional class. Risk-free must consequently be a relative term here: the DeFi risk-free rate will encompass substantially more risk than Treasury bonds. The former is always potentially vulnerable to smart contract failure, validator slashing, etc while the latter does not suffer any of these dangers: as an obligation from a government denominated in a currency that the same government is sovereign over, payment is guaranteed unless the US government intentionally decides to default on its own debt, which it is very unlikely to do (there is a broader conversation to be had about the plausibility of Treasury bonds being anything close to risk-free given the impact of reckless domestic US monetary policy on them, but that is ultimately a different topic). Suffice it to say that the crypto risk-free rate is relatively higher in risk than most other risk-free rates, and should have an accordingly higher floor of return to compensate.

The best theoretical analysis of crypto risk is found in Lily Francus’ three-part series. That series constitutes the most rigorous attempt yet to precisely measure the risk-free rate in crypto through an in-depth consideration of currency risk, hedging, and the perpetual basis trade. While admirable, Francus’ level of specificity is unnecessary for the purposes of our analysis. We seek the risk-free return not for its own sake, but on the basis of it approximating an alternative to passively providing liquidity on Uniswap v3. It follows that a major consideration for us is that our solution must be essentially set-and-forget. Any requirement of extremely active management that can’t be automated away for virtually no cost (even if otherwise risk-free) will render a solution unfit for our purposes, since passively providing liquidity on v3 by definition does not require active management. What we are looking for is a risk-free rate that broadly minimizes any protocol risk and prioritizes more proven forms of return (thus ruling out Anchor etc, as well as any speculative degeneracy), while maintaining this property of passivity.

Like the heathens we are, scrutinizing the nuances of Lily’s considerations can thus be bypassed in favor of extracting her conclusions. While the series is once again worth reading, I can broadly summarize its conclusions for the less intrepid reader. The risk-free rate she settles on, which is currency-specific, is nominal staking yield from a protocol such as Lido, minus inflation and diversified slashing risk (loss through staking with a malevolent or incompetent validator). In practice, this gets somewhat more complicated: there are FX rate hedging mechanisms involving perps which should lower the rate, Lido provides stETH tokens which can bear yield elsewhere in the DeFi ecosystem which should increase it, and Lido’s status as a fast-growing monopoly could have second-order effects that drive the rate in either direction over time.

For simplicity’s sake, we’ll make the assumption that Lido’s APY will remain fixed in the future (in practice, there are plenty of reasons it could go up or down, but we’ll ignore them for now). Likewise, ETH may well become deflationary once PoS has been fully implemented, though it remains slightly inflationary at the present moment: we will thus assume that inflation is 0% in the long run, as we will also do with slashing risk, which should approach zero as rogue validators are eliminated. So the risk-free rate comes out, rather cleanly, to Lido’s current APY, which is 3.8%. To the members of the audience bursting to interject about funding rates and slashing insurance, our lack of hedging has precedent: the risk-free tradfi rate is not calculated as the Fed Funds rate minus a credit default swap, but simply the former. Since we are only looking for a close approximation, there is no need to include hedging costs.

We find the passive risk-free rate in crypto to be ~3.8%. Any strategy that underperforms this return is simply irrational (absent of second-order effects - something akin to Paradigm providing large amounts of liquidity to Uniswap at a loss to the risk-free rate, but ultimately profiting through taking advantage of expanded opportunities for MEV via the increased transaction volume enabled by their liquidity provision). There are no second-order effects available to retail users, only to institutions: retail underperformance of this rate is irrational without qualification. In particular, we note that this is a passive return. Outperformance of this return is not simply a function of increased profit, but increased profit and a similar level of passivity: if a position must be heavily micromanaged to eke out a ~4.5% risk-free return, its superiority is highly questionable. Markets are not perfectly efficient, but in the long term, absent a secular decline in staking and lending returns, we can expect market participants to demand this payout as a minimum for the services of their capital. If v3 liquidity providers are not reliably receiving this payout, then liquidity will exit the protocol to seek returns elsewhere.

Recap of Uniswap v3 LP mechanics

A brief review: Uniswap is a prominent example of the class of decentralized financial primitives known as AMMs, or Automated Market Makers. Given the extensive costs that come with space on the Ethereum blockchain, the costs of a decentralized order book exchange were prohibitive: the mechanical and computational difficulty of representing the totality of the bids and asks in a smart contract, if at all possible, was costly to the point of infeasibility. AMMs thus do not function like an order book, which centralized exchanges use. In other words, there are no bid-ask spreads or market makers who provide liquidity. The liquidity instead comes from providers who deposit liquidity into pools at a 50:50 ratio, in exchange for receiving a fixed percentage of trading fees in the pool. Uniswap v2 became the undisputed king of AMMs, allowing users to deposit liquidity and receive trading fees for the service of their capital. Liquidity provision on v2 was ambient: it was equally distributed across the entire distribution/sample space of price points, allowing for no customisation of price ranges to set liquidity within. The profitability of a given Uniswap position depends entirely on the quantity of trading fees occured vs impermanent loss suffered. If the former is greater, the position is in profit, and vice versa: the larger the delta, the greater the profit or loss respectively.

Any deviation in AMM pricing from the spot price on centralized exchanges is quickly resolved through arbitrage: liquidity on v2 was consequently being provided at price points that in practice virtually never required it, such as <$500 or >$8000 for ETH when it was at $3000. The inefficiency of this design became clear through a series of developments including the rise of Curve, whose StableSwap invariant design (x+y=k) allowed for much cleaner stablecoin swaps than Uniswap v2’s x*y=k formula, and consequently dominated that segment of the market.

Curve vs Uni v2

Uniswap thus introduced v3, which enabled range-bound liquidity: it allowed users to select price ranges to provide liquidity within. This update brought stunning composability gains, allowing v3 to simulate nearly any static AMM. While this enabled v3 to compete with Curve and theoretically made liquidity provision drastically more efficient, it also introduced externalities which have only become evident as time has passed. In particular, v3 has been marketed as the cutting edge of capital efficiency. A key theme underlying what follows is that capital efficiency is a rather ambiguous term: there is a universality to it which implies that the efficiency has accrued to both swappers and LPs, but in reality that efficiency is drastically one-sided.

Selecting price ranges for your liquidity effectively amounts to leveraged liquidity provision vis-a-vis ambient liquidity provision, with all the consequences leverage entails. While gains are magnified, the margin for error shrinks proportionately: impermanent loss can be much more punishing than when the user was forced to provide ambient liquidity. This leverage poses many dangers for a passive, retail LP: the more concentrated the liquidity position, the slimmer the margin of error before impermanent loss rears its head. An intuitive way to think about impermanent loss is that, as one of your assets appreciates relative to the other (say you’re LP’ing in the ETH/USDC pool in the $1800 to $2200 range, and ETH goes from $2000 to $2200 while USDC naturally remains at $1), you are forced to sell the over-performing asset for the under-performing asset i.e. as ETH’s price goes up relative to USDC, you are forced to sell ETH for USDC, limiting your upside. Conversely, if ETH depreciates from $2000 to $1800, you are forced to sell USDC to buy ETH, exacerbating your downside.

There are many technical ways of making this point: Uniswap LP positions are inherently short gamma, the graph of their payout is concave, not convex, and so forth, but the point can be summarized in a completely non-technical manner: large movements in either direction are bad for v3 LPs due to the aforementioned mechanics of impermanent loss. The LP is hoping for high volatility inside his price range (to accrue trading fees), but little to no movement beyond it (to avoid impermanent loss): since crypto is a dramatically volatile asset class, this is a very unreliable aspiration. Sudden sharp moves, par for the course in crypto, are inherently bad for LPs: in particular, any sharp move will cause a position with passive range selection - the hallmark of the retail LP - to first suffer IL and then remain permanently out of range, thus accruing zero trading fees. Intuitively, we might think that the longer the position is passively held, the greater the probability it will suffer this fate: this intuition proves partially correct.

However, auto-rebalancing may well underperform passive LPs in this scenario, since rebalancing crystallizes losses and costs gas. If the price of ETH appreciates and auto-rebalancing occurs, and the price then reverts to the mean (provoking another auto-rebalancing), there has been no compensation for multiple gas fees and crystallized impermanent loss: clearly scenarios exist where auto-rebalancing is significantly inferior to passivity. Do active LPs generally outperform passive LPs? Is there a time period within which it is particularly perilous to crystallize impermanent loss through rebalancing? To explore this and other questions, we will now examine the empirical reality of v3 liquidity providers.

Empirical review of v3 LP profitability

0xfbifemboy’s four-post series on liquidity dynamics on Uniswap v3, a extension of Loesch et al’s paper Impermanent Loss in Uniswap v3 (2021) with particular focus on the ETH-USDC pool, is not only a must-read but also the most extensive of a series of analyses (Rekt, etc), all of which concur: providing liquidity on Uniswap v3 is, broadly speaking, unprofitable vis-a-vis simply holding the position without providing liquidity/outside of Uniswap. In other words, the hope of Uni LPs that their position will accrue trading fees that outweigh impermanent loss is empirically unjustified: ~50% of LPs are losing money relative to simply holding the assets. There is little to no empirical evidence to the contrary.

In the first post, the author notes that while the median return of APE/ETH LPs was exactly breakeven (due to many positions incurring zero IL and gaining zero fees due to being permanently out of range), the average position lost 3.8% of their initial. With our absolute risk-free rate in crypto also at 3.8% (similarity to APE/ETH loss of initial is obviously coincidental), the situation becomes even worse: the average APE/ETH LP not only lost almost 4% of their initial but also the risk-free return, with a long tail of LPs losing substantially more. As we had hypothesized, the length that an APE/ETH position remained open was strongly correlated with a higher degree of impermanent loss, demonstrating the pitfalls of passive liquidity provision on v3.

However, APE/ETH may well be a sui generis pool: not only new, but linked to NFT performance in ways that may be unrepresentative of v3 pools at large. Thankfully, more generalized analyses exist. Per Bancor, 80% of the many pools surveyed lost more through impermanent loss than they received through trading fees. If the ability to not only hold the assets outside of v3 but also stake them at the risk-free rate of 3.8% had been added to this analysis, that figure would likely have risen to somewhere around 90%. While it is true that there are not risk-free rates for every currency as there is for ETH with Lido, the overwhelming majority of LPs losing money in this fashion is nevertheless a calamitous result. As a follow-up to the correlation of length and IL in the APE/ETH pool, the length of the positions in these pools initially correlated with IL loss, but then declined: positions held for a month had a significantly more healthy IL-to-trading-fees ratio compared to positions held between an hour and a week, which is one form in which the APE/ETH pool may not have been representative. The correlation between position length and IL thus forms an inverted-U shape. However, Lambert found that narrow-range positions accumulate trading fees proportionately to the square root of the time held of the position, causing returns to diminish over time: it takes progressively longer to double your trading fees. The decreased IL of long-term positions may not overcome the diminished trading fees that result from those positions, incentivising frequent exiting of positions.

Position length and trading fees

One claim made by supporters of the Uni v3 model is that v3 is always better than v2 because you can at worst simulate the ambient liquidity of the v2 model on v3 by setting your liquidity from [0, ∞). At a brute empirical level, however, large amounts of concentrated liquidity alongside passive ambient liquidity is not replicating the v2 ecosystem, since LP profits are getting squeezed in a manner that simply was not occurring prior to v3. The theoretical claim that synthetic v3 ambient liquidity recreates v2 ambient liquidity must then be incorrect, but this should not surprise us: v2 ambient provision also stipulates that everyone else must do the same, whereas v3 does not, significantly altering the game-state for all of its participants. There is no obvious reason to assume that this change would not have an impact. Moreover, not all improvements are Pareto improvements: they often carry tradeoffs, so it should not be particularly surprising that v3 may well have tradeoffs that compromise LPs in exchange for aiding swappers.

The Rekt article poses a pointed question: liquidity provision wasn’t broken, so why did they “fix it?”. This touches on what is perhaps the crucial point for understanding the current state of affairs: v3 was an update motivated not by improving the situation for LPs, but for swappers. I believe the logic for Uniswap v3, cold and unyielding, can be found in the depths of Twitter disputes on the topic: per Hayden, since v3 is the most capital-efficient market for the buyer, all non-arb volume should in time flow there instead of v2, thus incentivising LPs to move as well and eventually killing v2. If v3 did not provide this extremely buyer-friendly model, a competitor would emerge who does, and no-arb order flow would rotate there instead of Uniswap. In other words, in the long run LPs are going to get squeezed regardless, so there is no virtue in waiting for a competitor to make the first move.

While the game theory checks out, the fact remains that there is neither theoretical nor empirical justification for the accompanying claim that passive LPs always do better on v3 than v2. Capital efficiency for swappers has significant externalities for passive LPs. Notably, 0ff found that if all APE/ETH liquidity providers had provided ambient liquidity instead of bounding by range, they would have cumulatively suffered significantly less IL. This is because profitably LP’ing on v3 requires a sophisticated understanding of volatility and directionality in order to set an appropriate range that has repeatedly proven beyond the capacity of the average LP. An appropriate degree of understanding of these factors is almost by definition impossible for passive LPs, who definitionally do not micromanage their positions this way.

There are obvious ways this situation can further deteriorate: for one, if HFT firms enter the market and begin actively LP’ing with ML-trained models, passive profit will further contract. At this point JIT-style MEV is usually mentioned in the conversation. That issue will be considered in a future post all of its own: the tl;dr is that it’s not as worrisome as many have claimed, and measures already exist that can mitigate it, though they haven’t yet been widely implemented. Allowing JIT would thus be a design decision rather than an unavoidable hazard: other forms of MEV are less remediable through design.

Liquidity Provision in a v3 world

0ff argues that while “the lack of overall LP profitability is a problem, it is a resolvable problem”: through mechanics such as “merging fee tiers, automatically modifying pool parameters, or guiding LPs to set appropriate position ranges”, the problem can be substantially reduced. This seems overly optimistic. The first two proposals are vague enough that it is difficult to address them without further specification: auto-modifying parameters, for example, would likely be much more gas-efficient on CrocSwap than v3 due to differences in the underlying design, so while they are potentially viable it is difficult to discuss them further without concrete implementation. In terms of the latter suggestion (LP guidance) 0ff’s very own analysis has shown that there aren’t obvious patterns differentiating big winners and big losers other than the former (such as 0xB0b) happening to LP around a price point that proved to be very sticky i.e. ETH at $3200. If generalizations about the tendencies of profitable LPs cannot be made, then it is for now impossible to create a tool for passive LPs that can improve their range setting. As will be discussed below, the author’s intuition is roughly correct: there are tools that can mitigate the problem, but the Uniswap team has thus far proven singularly unwilling to countenance their integration.

More broadly, the Sommelier Finance team has stated that even when running a backtest where they knew the end price of the token in advance, they still ended up losing money, presumably because rebalancing locks in impermanent loss and costs gas. This is an extremely pessimistic thought, suggesting that there may in fact be deep structural reasons why v3 LPs are broadly unprofitable, such as an overly-elevated lower bound proportion of toxic flow to non-toxic flow. A more optimistic interpretation is that the colossal amounts of IL stem from an oversupply of liquidity to certain pools, which causes an increasing proportion of order flow to become toxic. The solution, then, would be to develop tools which inform LPs when their pools are oversupplied. In theory, this might be possible: it is intuitive that the relative quantity of IL in a given pool (which can be calculated at any time) could be a direct indicator of whether the pool is oversupplied or not. However, per Loesch, very many pools in v3 exhibit these IL characteristics, rather than just extremely large pools such as ETH-USDC (0.3%), which suggests either that oversupply is not the relevant metric or that v3 pools are systematically oversupplied. The chart tells a sad story:

v3 pool profitability

Several solutions have been proposed to the problem of ~50% of Uni v3 LP positions being unprofitable in relation to simply holding the assets. The most prominent are discussed below. As I stated in the introduction, these solutions are theoretically capable of aiding LPs, especially if Uniswap migrates to Optimism, but lack empirical evidence of efficacy and any kind of clean integration with v3, rendering them uncertain and unwieldy.

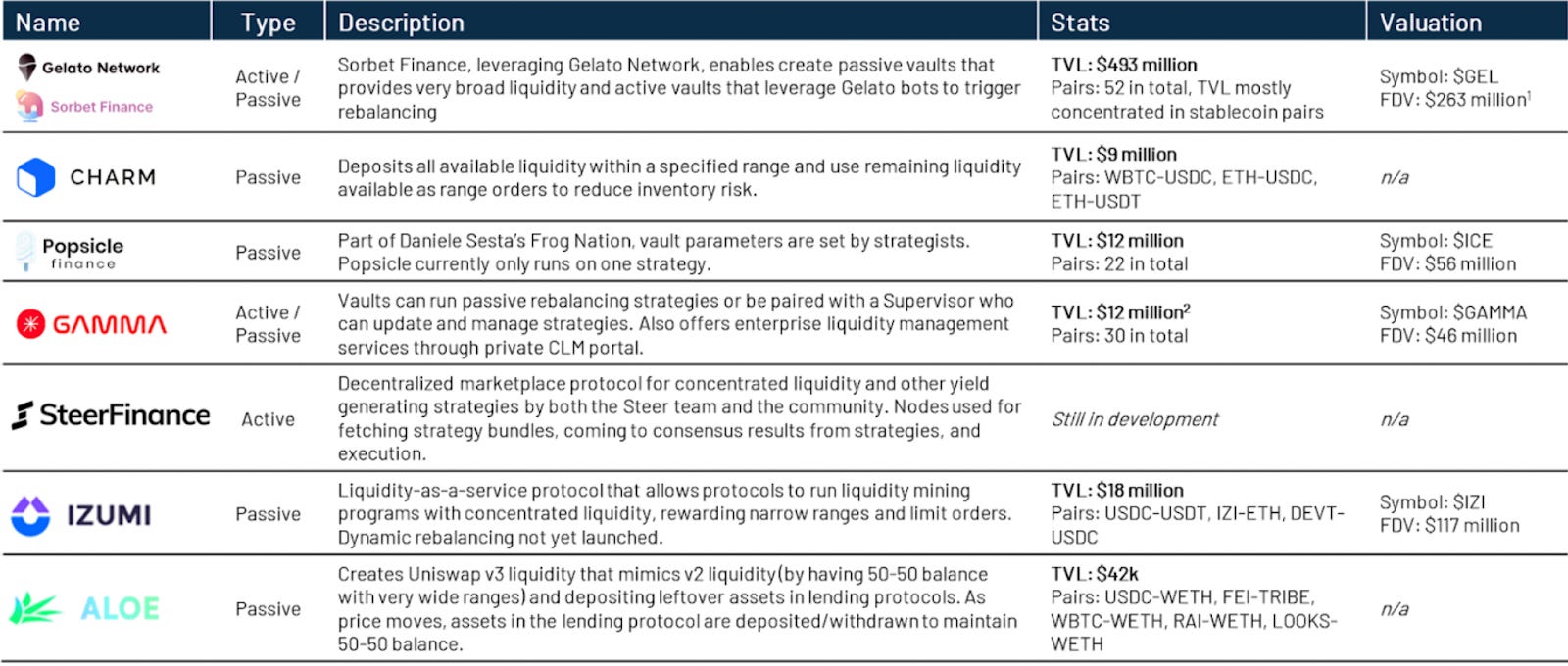

Active Liquidity Managers

The first solution is Active Liquidity Managers (ALMs), such as Gelato, Popsicle Finance and the much-vaunted Visor, which later merged to become Gamma. These protocols claim to actively manage your liquidity for you in a variety of ways, most revolving around rebalancing in order to keep your position in range, so as to prevent your capital from accruing no trading fees. In theory, this aggregate readjustment should be vastly more gas efficient than individual LPs all readjusting their positions, and some empirical evidence exists to bolster this hypothesis, with the significant caveat that the protocols have almost always themselves carried it out. However, both Loesch and 0ff call into question the viability of this strategy. If there are no clear behavioral patterns (such as position length) by which the most profitable v3 LPs differentiate themselves from the least profitable, nor any empirical evidence to suggest that actively managed LPs outperform passive LPs, then there is no reason to think ALMs generally outperform passive LPs. Aside from potential issues of scale as a given ALM’s TVL increases, ALMs have best product-market fit in a world where active LPs dominate passive LPs, perhaps in an oligopolistic, tradfi-MM sense. If the limiting factor of retail LP profitability was willingness to actively manage their positions, ALMs would have a real raison d’être. Since this is simply not the case on v3, ALM advantages are vastly reduced - even before they take management fees! To reiterate: ALMs must not simply outperform retail, they must outperform the risk-free rate (4-5%) after management fees. At the moment of writing the writer could not find a single empirical datum suggesting that ALMs consistently outperform retail v3 LPs before management fees, let alone after: a fortiori they drastically underperform the risk-free rate for the time being.

ALM overview

As mentioned before, the Sommelier team lost money even when they knew the end price of the token in advance, as rebalancing not only costs gas but also crystallizes impermanent loss. Without further details of the team’s backtest, authoritative judgements cannot be made on the ratio of importance between the two, but if gas is the main cause of ALM strategies failing, the migration of v3 to layer 2 solutions such as Arbitrum may well redeem the viability of ALMs. However, if impermanent loss is the prime mover, the problem remains.

Moreover, empirical evidence for ALM outperformance on L2s is sorely lacking: one wonders if the teams behind these protocols are simply incompetent at publicising their outperformance, or whether their silence signals that their product simply fails to perform as advertised. There may well be underlying reasons for the absence of this research: any public strategy that notably outperforms the average LP position on v3 over a non-trivial period of time would have to be proprietary (i.e. private), since if it were public, it would either be replicated or front-run into oblivion. But as the blockchain is inherently public, any act of rebalancing requires gas, is public, and replicates other features common to transactions (is this true?). It may be the case that ALMs are inherently incapable of moats: any inefficiencies they find in the LP market which allow for consistent outperformance will be tracked and copied, arbitraging away the intellectual premium. If they somehow avoid this fate, hiding themselves in a corner of the dark forest where predators do not frequent, they will not be keen on advertising their outperformance: but without empirical evidence, we have no reason whatsoever to trust their claims of efficiency.

In terms of outside research on the profitability of certain v3 strategies, both DeFi Scientist and Neuder et al. have published interesting analyses examining the profitability of certain v3 strategies. An assumption made for the purposes of complexity reduction in both of these works, however, is that every other market participant is providing v2-style ambient liquidity. I am sympathetic to the necessity of the assumption, but must admit that I am not sure how applicable either of the papers are to a world in which virtually everyone is providing range-bound liquidity.

Squeeth

Squeeth almost perfectly hedges Uni v3 LP positions. Providing liquidity on Uniswap is short gamma, since large moves in either direction disproportionately hurt you: more broadly, the nature of LP’ing is a gamble that the trading fees received outweigh the fact that you are selling volatility i.e. that large moves will not occur. Amongst its other applications, Squeeth hedges IL through acting as long gamma, and has other desirable properties such as its lack of rollover. It is a rather novel primitive, and the Opyn team should be commended for its development.

However, despite its technical innovation, Squeeth has practical drawbacks. It is rather unwieldy for the passive retail user: hedging v3 impermanent loss involves purchasing oSQTH with the same gamma as the Uniswap pool before selling ETH perp futures to hedge ETH itself. On a once-off basis, this might be achievable, but as the frequency of rebalancing increases, it becomes drastically less viable for the retail user. While Squeeth works better than ALMs, the bar for passive LPs is not breaking even: it is outperforming the risk-free yield rate. As before with ALMs, there is no empirical evidence that demonstrates v3 positions hedged by Squeeth outperform the risk-free rate. Running this kind of backtest shouldn’t be that challenging: the Squeeth team’s failure to do so is rather strange. Absent further evidence, my intuition is that outperformance of the risk-free rate is unlikely unless Uniswap subsidizes Squeeth purchases/funding rates. Perhaps the Squeeth team disagrees, but the burden of proof falls upon them to show it.

Nevertheless, Squeeth does not have some structural flaw that renders it unusable, as ALMs may have: the product is sound. However, my personal opinion is that the team is filled with very intelligent mathematicians and builders (such as the ineffable Wade Prospere) whose understandable enthusiasm for its fascinating properties have prevented them from effectively marketing it to v3 LPs, particularly of the passive variety. The language of gamma and funding rates is not particularly transparent to these users, and if Squeeth positions themselves require manual re-adjustment, the problem is only compounded. The solution to the product’s opacity is providing a tool by which it can be cleanly integrated into v3 LP positions in a few clicks. As we will discuss below, however, the Uniswap team is at best indifferent to this problem and at worst nakedly dismissive of IL (and hence of the necessity of automated hedging such as Squeeth) so no progress has been made on this front in months.

Alternative AMMs

Certain design features of AMMs may mitigate the problem: CrocSwap’s fascinating design of placing the pools inside a single smart contract might well yield dramatic increases in gas efficiency for LPs. However, with v3 migrating to Optimism, that advantage is unlikely to prove particularly durable. One upshot of CrocSwap’s design is that the trading fees auto-compound, which was a feature of Uni v2 but not of v3 (due to the latter’s switch to an NFT-based position structure), forcing its LPs to manually compound the trading fees. While a nice feature, auto-compounding is unlikely to significantly affect LP profitability.

Other AMMs claim to idiosyncratically protect their LPs from IL, such as Bancor 3, through maximizing passive yield and preventing IL through insurance provision. Bancor v2’s IL prevention mechanism provided 1% cover per day, with liquidity present for 100 days receiving full cover, which conveniently incentivised sticky liquidity alongside protecting LPs. This protection unfortunately came at the expense of the protocol incurring substantial costs: providing insurance is costly in the aggregate, cutting into the already-thin margins of DEX profitability. According to Loesch, v3 LPs incurred $260m of IL over 4.5 months, which would be $693m yearly. Intuitively, this seemed virtually impossible to fully subsidize in the long-run to me, though Bancor’s attitude of protecting its LPs was nevertheless admirable. Remarkably, Bancor 3 (currently in beta) offers full IL protection immediately, with the mild caveat of a 7-day cooldown period, which would seem even more unprofitable than v2.

However, Bancor v3 is an interesting case study that provides us some much-needed perspective on Uniswap v3 design choices. As a regulated Swiss non-profit, Bancor doesn’t seek rent extraction, but only to break even. According to the Bancor team, who have no obvious reason to lie since proof is empirically available if requested, they have in fact broken even on IL insurance since mid-2021, via insurance premiums paid by liquidity providers (constituted by a mixture of fee collection and innovative BNT-burning tokenomics). Moreover, many of the Uniswap v3 design decisions were anticipated by Bancor: they trialed concentrated liquidity in April 2020 in beta, before reverting due to the exacerbated IL the mechanic caused. This is a remarkable finding: it implies that increased IL is a direct and obvious consequence of v3-style capital efficiency, one which the Uniswap team would have quickly discovered in their own beta testing for v3.

Since a lot of AMM volume is HFT arbitrage, it might be more profitable for HFTs to subsidize IL rather than see liquidity exit en masse. If Han et al’s argument that order flow toxicity on Binance increases alongside Uniswap liquidity provisions holds, it might also make economic sense for Binance market makers to contribute to the subsidy. If Bancor was to engage in diplomacy with HFTs and MMs and successfully receive subsidies from them, the long-term viability of IL insurance would vastly improve. We see a recurring theme here: if sufficient empirical evidence can be produced, the situation can be addressed and improved, but this research does not exist and no effort is currently being undertaken to make it happen (though of all the protocols critiqued here Bancor is the least deserving of opprobrium: they have funded top-class studies in the past). As a rule, protocols attempting to mitigate IL appear to be chronically understaffed in the data analyst department and unwilling to contract Dune wizards to ameliorate the issue. I am not sure why this is the case, but it is an undeniably chronic problem.

Bespoke solutions.

Andre Cronje, whose reputation has recently nosedived after a dubious call for increased regulation, once proposed an impermanent loss insurance market, which Gamma endorsed. As far as I can tell, no work on this was ever carried out: whether the model was economically viable was never investigated in a rigorous fashion, and discussion about it has been non-existent for at least half a year. Having secured his bag and exited, Cronje is unlikely to do it himself: we await a hero to take up the burden.

In a somewhat similar vein, Lambert has argued that since v3 positions are analogous to short puts, a lending market for v3 “options” would likely increase the yield liquidity providers receive (since, given certain assumptions, it is almost always better to lend this position than hold it). Once again, no progress appears to have been made. Uniswap grants towards either of these measures would surely be productive: both are prime candidates for improving the quality-of-life of v3 LPs.

There may be some evidence that detection of pools where LP’ing is currently unprofitable is possible via comparing implied pair volatility to APY. But of the pools that remained profitable, most were small and thus vulnerable to new entrants, and tended to have less reputable pairs, exposing the LP to counter-party risk not present in pools such as ETH/USDC.

Implied volatility and APY

Conclusion

As discussed above, there is an imperial mentality to Uniswap v3: if we don’t provide the most efficient possible experience for swappers, someone else will, and swap volume will follow. While this sentiment has not always been made explicit, it is tacitly axiomatic among v3 experts. With Hayden proving extremely reluctant to even admit that there could be downsides to the update, the v3 experience seems nakedly hostile to LPs. The coldness of that mentality appears to have metastasized into inexplicably poor UX decisions. Uniswap doesn’t even attempt to protect its LPers from impermanent loss, whether through encouraging the usage of applications such as Defi Lab prior to entering a pool, or explaining the hazards of impermanent loss, its historical impact, and methods of hedging it such as Squeeth. Nor has any useful tool, such as a bot that can determine with reasonable accuracy if a pool is currently oversupplied with liquidity, been implemented or even proposed: that has been left to the Popsicle Finance team, who believe that their Sorbetto Limone tool can provide this service. But Limone’s development appears to have stalled, judging from the team’s lack of updates: there is no timeline for when it will be usable, and the Uniswap team has made no effort to either fund it or accelerate its development. This apathy is a chronic problem, a systematic feature of their approach to the ecosystem. It costs their LPs hundreds of millions per year.

This laissez-faire philosophy is an unforgivably poor design choice. Uniswap is by far the largest AMM in all of crypto with substantial institutional backing: its unwillingness to protect its LPs, whether by substantially contributing to empirical research which might narrow down the problem or providing forms of insurance/rebate through subsidized and automated hedges, has created an extremely adversarial environment for LPs. Providing the capacity to automate hedging for a given position through, say, a one-click Squeeth purchase should not prove particularly technically burdensome: its absence is less a product of infeasibility than Uniswap’s complete apathy towards the health of its passive LPs. If there is one takeaway from this piece, it is that Uniswap’s very admirable philosophy of improving the experience of swappers has not been extended to its LPs, who have been completely thrown to the wolves. We have briefly considered the possibility that Uniswap might need to subsidize IL, but since they are unwilling to even provide tools to detect it, this is currently a non-starter.

The solution to the problem explored here is simple: a vast quantity of further research, most of it empirical, is required. The possibility of tools that can detect when a pool is oversupplied with liquidity remains an open question; ALMs such as Popsicle and Gamma need to demonstrate the superiority of their product on L2s; Squeeth needs to do the same on the base layer; markets for lending and IL insurance must be explored. While Uniswap can be criticized for not attempting to integrate these solutions, the fault ultimately lies with these protocols and a misguided mindset that is more bent towards theoretical demonstrations of their efficiency rather than data-heavy empirical proof. As argued above, these protocols are filled with very clever technical builders, but there is a corresponding dearth of outreach to the average v3 LP. It may well be the case that despite these flaws, Uniswap’s migration to Optimism will prove a silver bullet, allowing minute levels of rebalancing (which are not currently possible due to L1 congestion) for ALMs etc. that redeems LP profitability. But migration will not prevent impermanent loss: if the latter is the primary reason for this systemic unprofitability of LPs, then their numbers will shrink.

As of now, it appears that most pools in Uniswap are oversupplied: that liquidity is simply not achieving the risk-free rate, and in time it will migrate. In theory, this exodus should continue until the average LP is earning ~4%, the passive risk-free rate. That will involve billions of TVL exiting Uniswap v3 over the next year. Where it will go is uncertain, but it will likely be an alternative which both surpasses the risk-free yield and does not allow for impermanent loss: Bancor 3, covered call SSOVs, LIDO staking, or similar. The former in particular may prove attractive because v3 positions closely resemble covered calls, albeit perpetual in nature. While buyers will, for the most part, find no difference between decentralized LPing and oligopolistic LPing, the decentralized vision of AMMs is heavily compromised if their liquidity comes to be mostly comprised by a few large market makers, as is often the case in TradFi. Philosophical questions emerge, but will not be considered, since this piece is already long enough: at minimum, the decentralized vision is heavily compromised if the leading AMM comes to resemble CEXs in its distribution of liquidity providers.

Regicide remains a distant hope for decentralized competitors. Uniswap v3 is a brilliantly optimized system, eking out almost unimaginable marginal gains for its users. Its capital efficiency, as marketed, is unparalleled - but that efficiency has accrued almost exclusively to swappers. The dark side of v3’s capital efficiency, the diseased child lying in squalid filth beneath Omelas, are the passive LPs of v3, who have empirically been punished by the update. Potential solutions, ranging from IL insurance markets to position lending markets to Squeeth automation and subsidies, have been totally ignored by the team, throwing passive LPs to the wolves. Hayden seems loath to admit the problem exists at all, while competitors such as Bancor and Euler lurk who understand the pain that subjects face. When kings develop contempt for large swathes of the governed, revolution has followed in short order.

—

If you enjoyed this post, please subscribe to my Substack for weekly content, and follow me on Twitter @semajeth. Thanks to 0xfbifemboy, Lily Francus, and Guillaume Lambert for their extensive work on v3, risk-free rates, and v3 derivations respectively, and to Mark Richardson of Bancor and Michael Bentley of Euler for their comments.

This is extremely well written, well edited. Thank you.

Thank you. Awesome article